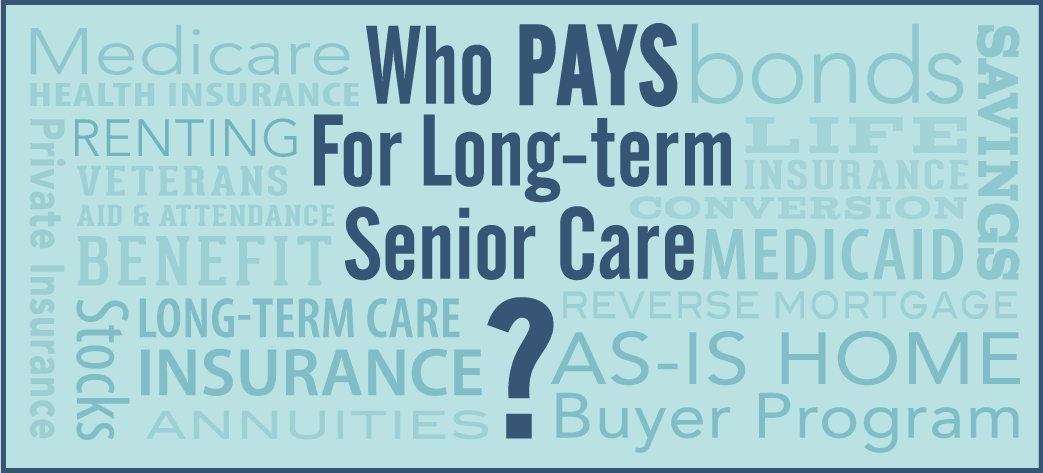

Fact vs Fiction: Who Pays For Long-Term Senior Care?

Fact vs Fiction: Who Pays for Long-Term Senior Care?

There are a number of reasons people don’t save as much as they will likely need for senior care. Unfortunately, one of the most common ones is the assumption that Medicare, Medicaid and/or private insurance will cover the bulk of your costs. Well, there’s an old saying about assuming that definitely holds true in this case. Learn fact versus fiction on who really pays for long-term senior care.

Senior Care: Fact vs Fiction

FICTION

Medicare covers all types of senior care for as long as you need it.

FACT

Medicare actually only pays for long-term senior care if you require skilled services or rehabilitative care:

In a skilled care facility for a maximum of 100 days. However, Medicare only pays 100% for the first 20 days.

At home if you are receiving skilled home health or other skilled in-home services as ordered by a doctor.

Medicare does not pay for non-skilled assistance with Activities of Daily Living (ADL), which make up the majority of long-term senior care services.

FICTION

Medicaid covers what Medicare doesn’t.

FACT

Medicaid does pay for long-term senior care both in a skilled care facility and at home. But to qualify, your income must be below the level set by your state and you must meet state eligibility requirements based on the amount of assistance you need with ADL.

FICTION

Health insurance offers more long-term senior care coverage.

FACT

Not really. Health Insurance through an employer or a private health insurance plan typically covers the same kinds of long-term senior care as Medicare.

Other Options to help you pay for senior care

Veterans Aid & Attendance Benefit

Wartime veterans or a surviving spouse with limited income may be eligible to receive a non-service connected pension (above the basic pension) to assist in paying for assisted living, home health care, adult day care or skilled nursing.

Long-Term Care (LTC) Insurance

LTC insurance can help you pay for home care, adult day care, assisted living, memory care, skilled nursing and/or hospice by covering services that health insurance, Medicare or Medicaid typically don’t.

Life Insurance Conversion

If you have an in-force life insurance policy you can convert it into a pre-funded financial account that disburses a monthly benefit to help pay for long-term care needs such as home care, assisted living, skilled nursing and hospice. What’s more, this account is a Medicaid qualified asset.

Reverse Mortgage

This is a type of home equity loan for homeowners 62 or older who want to access their equity to supplement retirement income. Here, the lender makes payments to you based on a percentage of your accumulated equity.

As-Is Home Buyer Program

Mom’s House is a national network of certified home buyers that purchases houses as-is for cash within weeks instead of months. They specialize in buying senior homes and offer an easier, less stressful option to sell your house without cleaning it up, cleaning it out or paying realtor fees.

And don’t forget to look at the resources you may already have available. We listed an option for selling your home above, but you might also consider renting it to help pay for senior care as well. In addition, do you have savings, stocks, bonds or annuities? How about Social Security income or a pension? Any or all of these can help you pay for long-term senior care.